The bank branch isn’t dead, it’s been re-born

There’s a commonly held view that Millennials, as digital natives, spend all their time online. Whether they’re socializing, shopping or banking, it’s all done via apps and social media, so bank branches must be a dying breed. In fact, the reality is more nuanced.

Rapid advancements in digital technologies, and an increasing number of channel options, are certainly changing how customers manage their finances. They’ve adopted digital channels, but they also expect branches to support and complement those digital services.

According to a global study from Bain & Company, 65% of consumers said they valued the presence of bank branches in their neighborhood. Even those who are happy managing day-to-day transactions online still value human assistance when it comes to making more complex decisions.

Think about it: if you’re faced with making an important, high value purchasing decision, such as applying for a mortgage or a student loan, would you rather scroll through pages of online technical specifications, or sit down with a friendly expert who can run through all the options and answer your questions?

Take Elsa as an example. She’s been living and working in London for seven years, but is now happy to be returning home to the Netherlands and a new job at a tech start-up. She’s also feeling a little over-whelmed because she has numerous financial arrangements to sort, out as well as settling into her new apartment.

Is this really a bank?

Elsa has generally been happy to do most of her banking online. But, now she feels she needs some guidance. She wants to open a new account, take out a credit card and, possibly, a car loan.

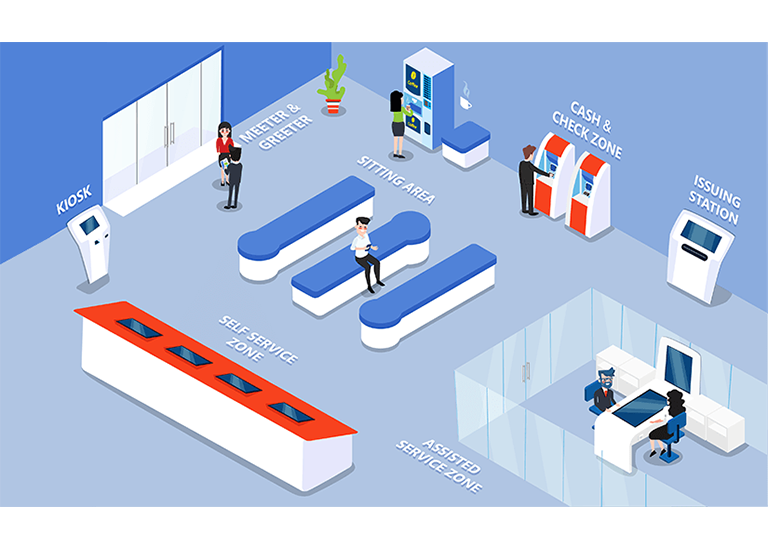

Like most of us, she hates standing in queues so she’s delighted to be able to arrange an appointment, at a convenient time and branch, using her mobile. But, that’s not the only surprise for Elsa. Everything about this branch looks different; it feels less intimidating and more inviting.

There are no tellers sitting behind glass screens. Instead, there are virtual meet and greeters that direct her to self-service banking zones with digital touch screens, where she quickly and easily sorts out her account and credit card application. She’s relieved the branch also has more private, assisted kiosks where she can talk to someone about her car loan.

Because the staff aren’t spending all their time dealing with day-to-day transactions, they’re able to give Elsa personalized advice about her options for car finance. The whole experience has been convenient, seamless and engaging. Elsa feels much more confident about her finances now she knows there are helpful experts always on hand at the branch when she needs them – and she even got to enjoy a cup of coffee.

Digital branches are a big differentiator for banks

Elsa’s experience is not a futuristic dream: combining digital technology with face-to-face consultations is already delivering major advantages for forward-thinking banks. Smart technology, such as self-service and assisted service terminals, and unified front-end systems for tellers enable paperless, straight-through processes. This can transform branch operations away from a low value transaction orientation to higher revenue, more customer centric sales and services.

Gulf International Bank is a successful example of this. They worked with VeriPark to develop and implement a paperless, digital branch concept, branded as ‘meem’. As a result, the time taken to open new accounts and approve loans has been reduced to just 15 minutes and customers only need to sign a simple, one-page contract.

The bank has gained 50,000 new customers in a short amount of time after implementing this rapid digital service. Transactions are now made via tablets and kiosks in branches that look more like Apple stores than traditional bank branches. This has not only reduced acquisition costs, it has also empowered customers and established Gulf International Bank as a trendsetter in the region.

Many customers want guidance and personal service from their banks. And, the most effective way to deliver this is often face-to-face. While the operational costs of traditional branches are a legitimate concern, introducing digital branches as part of an Omni-channel strategy alongside re-thinking the role of branch staff, can reduce costs, improve customer experience and boost profits.

Bank branches aren’t dead. But, they do need to change. If they’re to satisfy their customers’ desire for advice, personal service and security in complex and sensitive financial decision making, banks will need to develop branches that are inviting, customer-centric and efficient.